Coherus Oncology Current and Expected Returns.

One approved drug, LOQTORZI®, and a multi billion dollar pipeline. What are the actual Probabilities of Success, and what are the corresponding valuations.

Below, I will go over Coherus full cash position, pipeline, and potential as an investment, as well as an investment timeframe for both entry and exit.

Pipeline

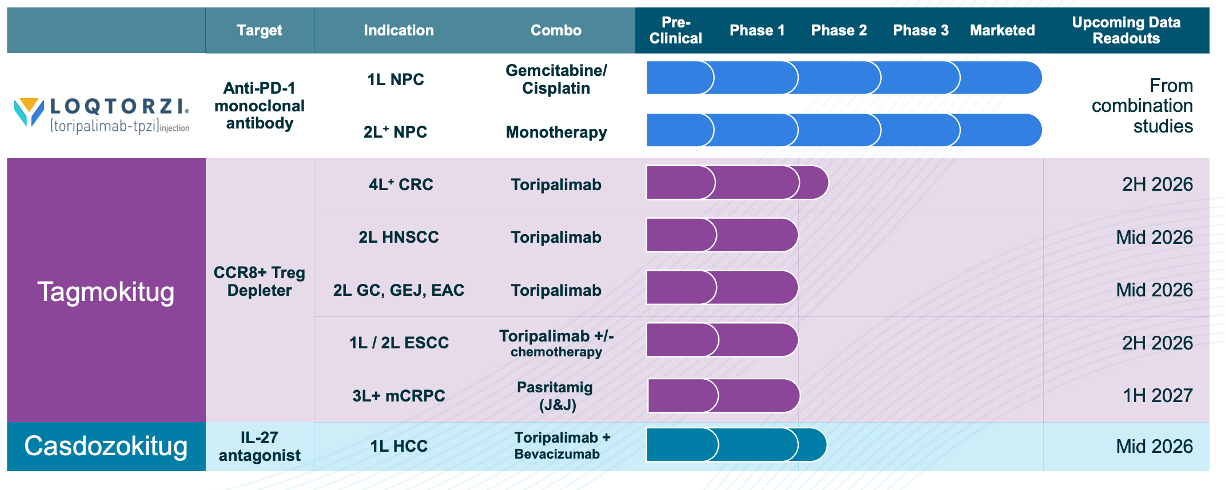

While this graphic from their presentation gives a good overview, there are still some caveats I want to discuss here.

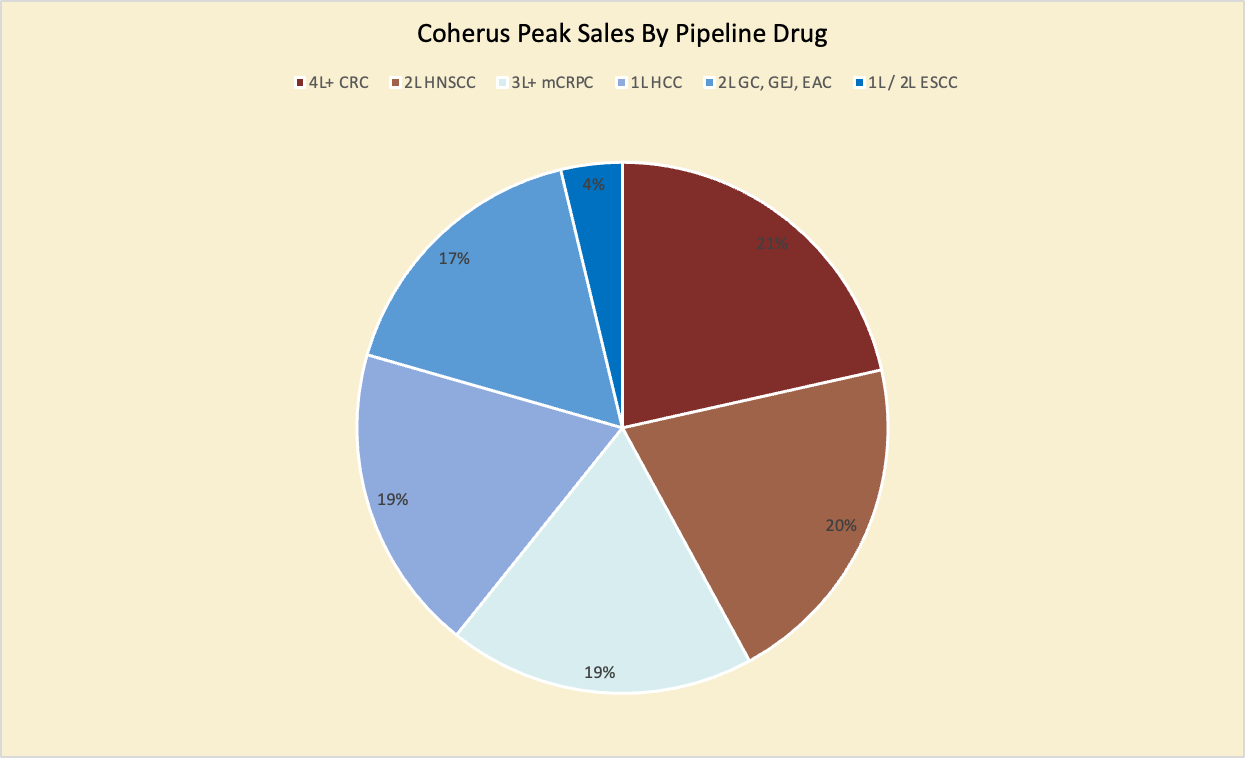

Below you can see the peak-sales distribution, with peak sales as the weight in the total pipeline peak-sales of USD 21.4 B:

What I find fascinating about Coherus is that its market cap is only USD 261 M. Even a Phase 1-to-2 advancement of one of their three 4 billion+ drugs, which is likely to occur in approximately 80% of cases, since the PoS of advancing from Phase 1 to Phase 2 is about 50%, could significantly boost the market cap.

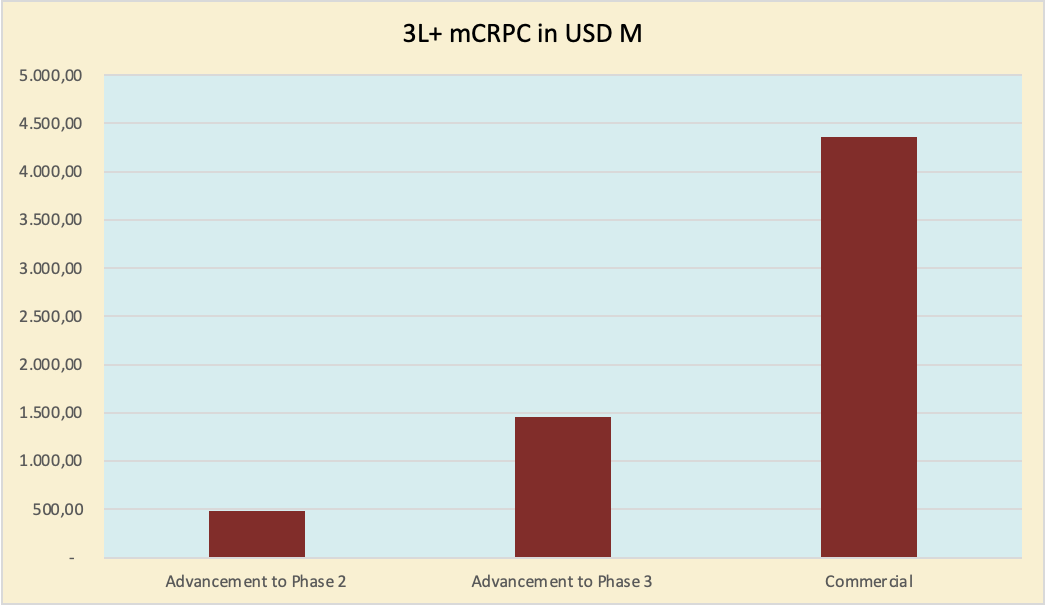

The graph below shows what the Phase 1-to-2 (and beyond) advancement of one of the Phase 1 drugs with peak sales of 4 billion would look like.

This is not the only case: as you can see in the distribution above, any of the high-peak-sales drugs could completely change Coherus’ market cap.

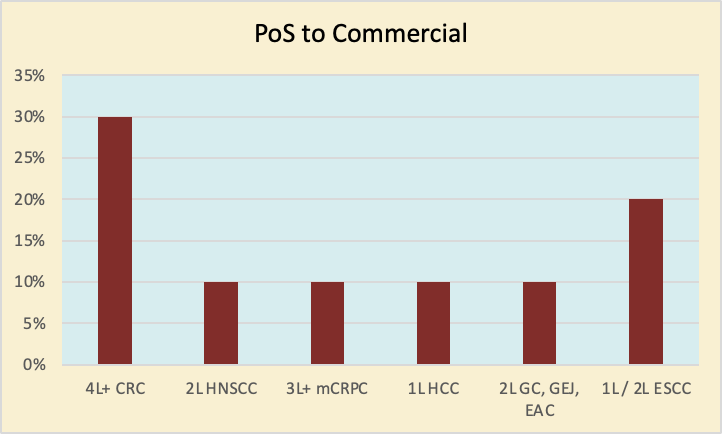

That, for the value, to go over the PoS of every stage and the efficacy of every drug would be too much for this article, but I made a graph showing each pipeline drug's PoS to commercialisation. I used these numbers for the DCF, and they are on the lower end because I would rather undervalue a company than overvalue it, and I like to invest based on probability-adjusted ROI. In reality, these numbers all could be 5-10% higher.

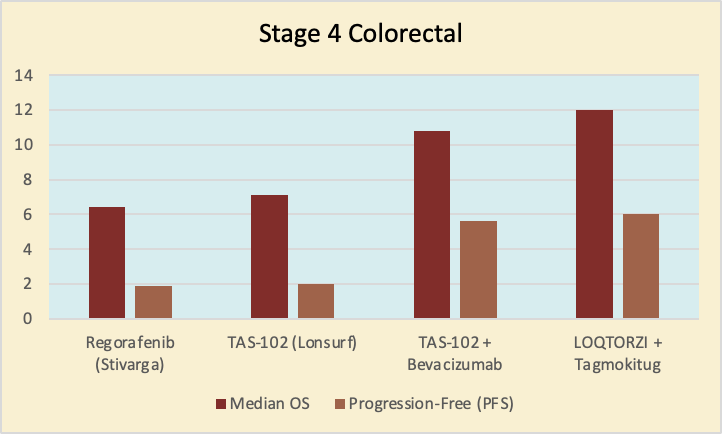

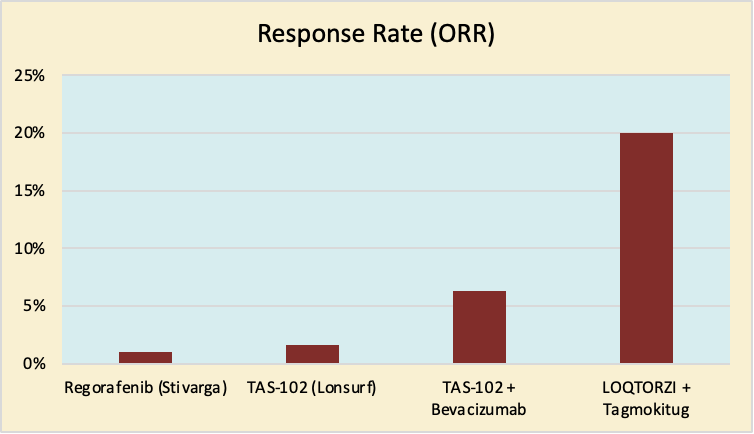

CRC

The article is already too long, and examining every drug like this would completely inflate its length, but I want to examine the two Phase II assets here.

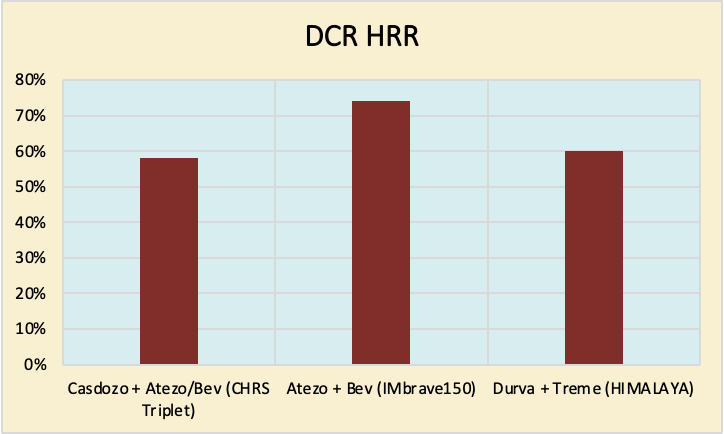

As you can see below, CRC is a double-edged sword for Coherus and should be used in specific situations, given that the OS and PFS are comparably low while the ORR is very high. (peak-sales: USD 750M)

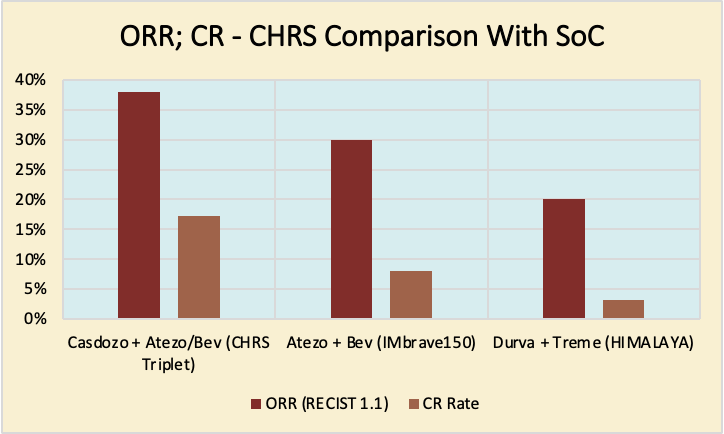

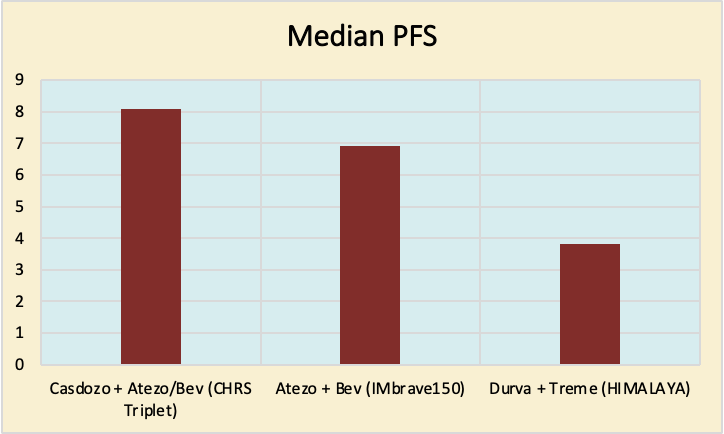

HCC

As CRC is a double-edged sword for Coherus, so is Hepatocellular Carcinoma. At USD 4B peak sales, this drug could have a profound impact on the valuation if it succeeds in Phase II. The drug's strength lies in the complete control rate, the objective response rate and the progression-free survival. Its weakness lies in the disease control rate. This essentially means their drug Casdo doesn't stop or slow down as many tumours, but it stops more tumours completely.

Cash Runway

Coherus is technically not just a clinical-stage company, but their only approved drug, LOQTORZI, is not profitable and, if continued at the same projections, will not reach profitability before the marketing expenses for their pipeline drugs are necessary; thus, I would largely value CHRS like a preclinical company.

Their current cash position will bring them through 2026, which is a data-rich year, as in the graphic above.

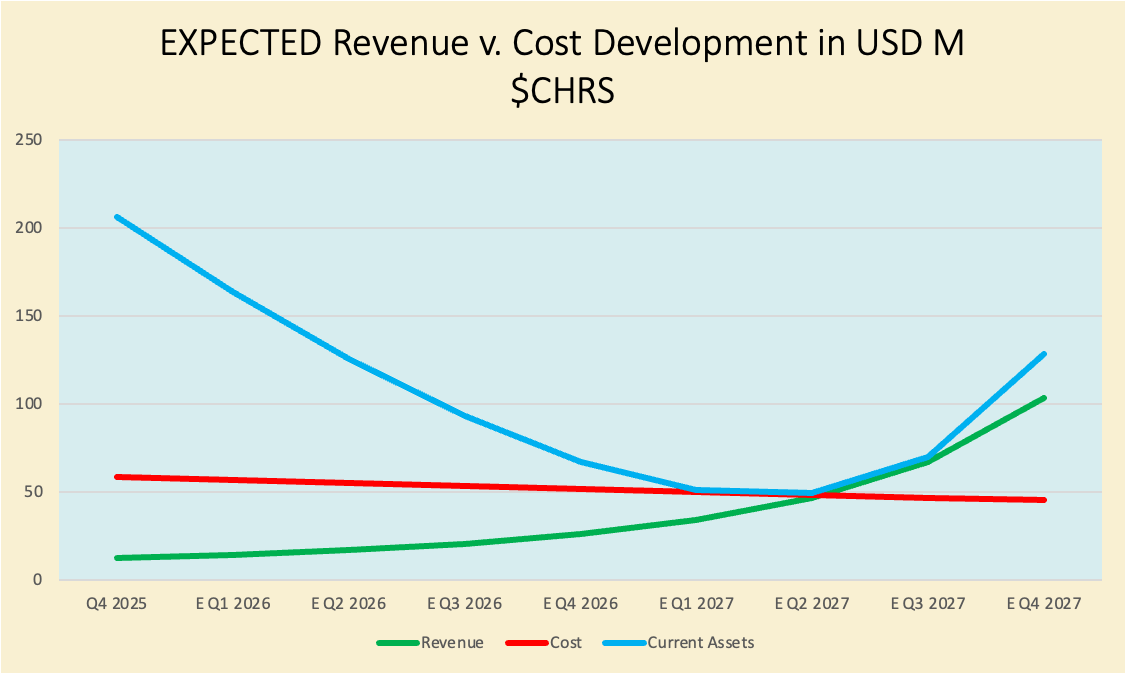

To visualise the situation, I first want to show what Coherus profitability of LOQTORZI’s looks like when isolated:

As you can see in the graph, with 15% YoY revenue growth and 3% annual cost reduction, the company would likely turn profitable without raising much, if any, additional capital.

Part of these cost reductions is due to lower interest rates. In a divestiture, they recently paid off almost all of their debt. They sold their UDENYCA (biosimilar) franchise for USD 558M, which they used to pay off their debt, reducing it from USD 480M to about USD 38.8M as of early 2026.

This is unlikely to happen, but it gives me confidence that in failed trials, the whole company would likely not need to be completely dismantled.

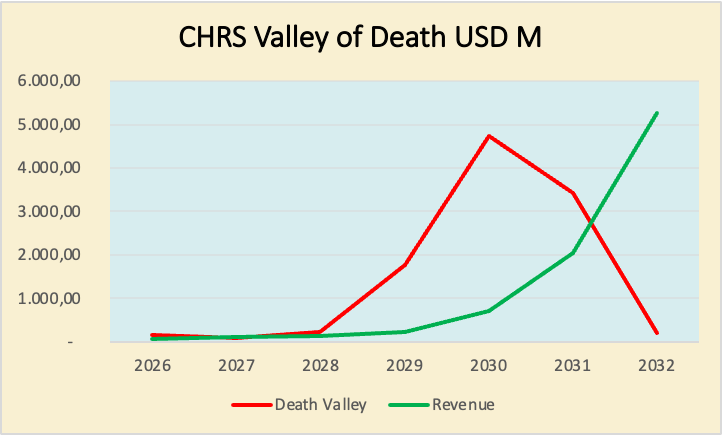

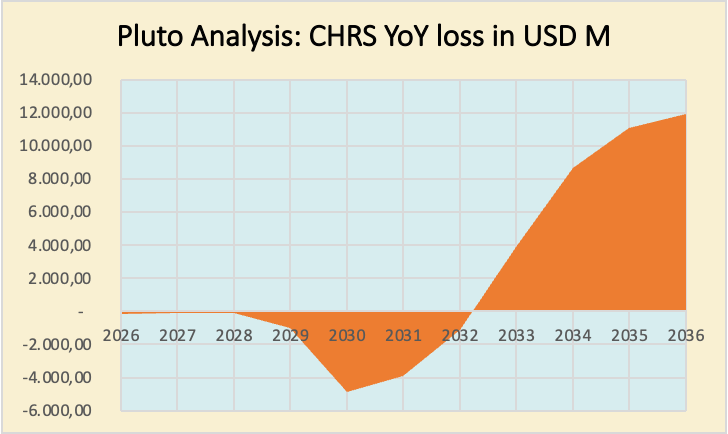

Here is some version of what could actually happen at a much smaller scale, since they are developing a massive pipeline of new drugs, which will sharply increase R&D and M&S expenses in the future. Coherus still has to leap over a huge valley of death. Their pipeline is actually so huge that this valley, compared to their current market cap, looks completely unrealistic.

In this graph, the red line shows the yearly loss, while the green line shows the corresponding revenue, which starts to cover losses in 2033.

Since Marketing expenses are usually expected to be 30% of the drug's peak sales starting the year of marketability, and 3% the year before, we can see a huge spike in expected spending when we enter 2029.

This exact scenario is likely not going to happen, but it paints a picture of the actual costs associated with their drugs and the need for either a massive partnership or outlicensing of some of their pipeline drugs.

Below is another graph of Death Valley, which shows their need for either licensing or an acquisition, and is also prompted by the CEO’s age, which I will discuss later.

Importantly, this does not yet include the necessary total R&D cost, which I will roll out in the valuation section.

Management

I will keep this short. In my Calculations, I use metrics such as outside tasks, public image, and experience to evaluate the quality of the CEO and management on a scale of 0 to 10.

On my scale, Coherus management scores 9,3 which is comparatively high. There are some other items that need to be addressed, though.

There is some uncertainty about a successor. Yes, the company is young, and yes, there are experienced people at Coherus, but given the CEO’s age and the situation they are in, this needs to be addressed in the valuation.

The CEO is 70 - this means he is likely looking for retirement, which is especially important considering that they are reaching a discounted valuation peak only in about 9 years, which means there is some time to accumulate.

I found an additional yearly 5% discount due to management risk, adequate for Coherus.

Valuation

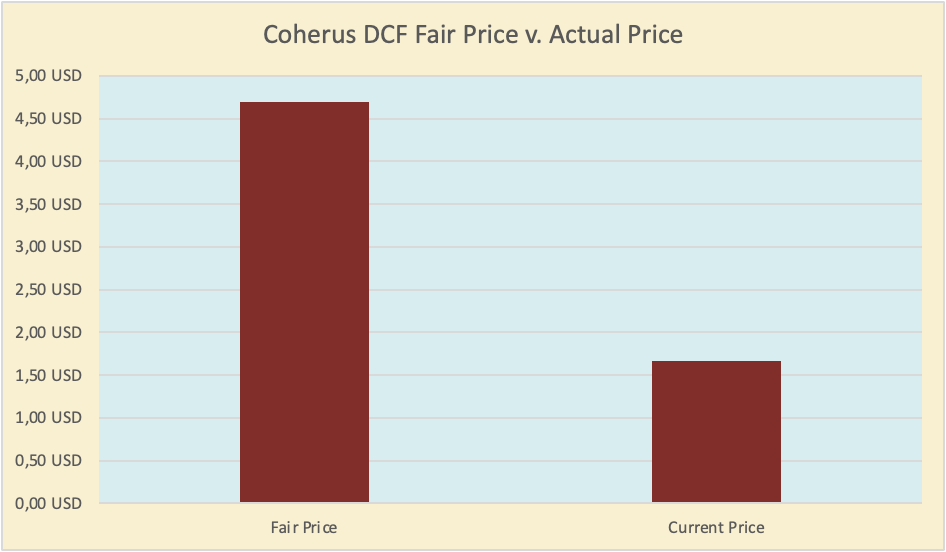

In my DCF, I found that Coherus is currently undervalued:

According to my DCF, a fair value for Coherus' share price would be 4.70 USD at the current stage, vs. 1.67 USD, the current market price.

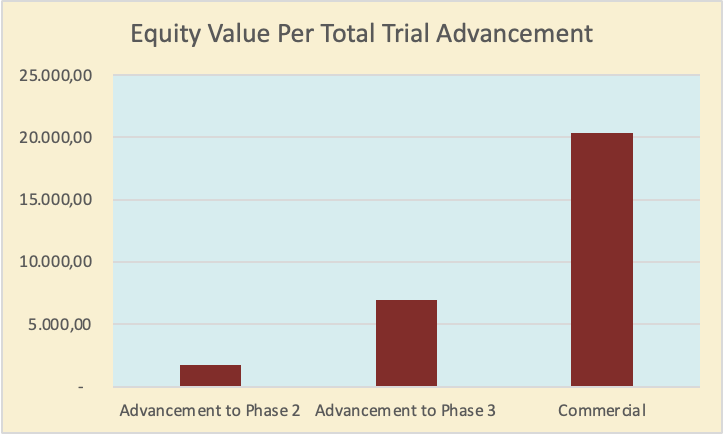

Now, there is some reasoning behind this discrepancy, which has to do with the funding issues I outlined above, as well as their recent divestiture of the biosimilar business. In the best case, they can quickly find a partner to out-license one of their products for Biobucks and Royalties, or they get acquired soon after major Phase II and III advancements. Below, I made a graph outlining potential acquisition prices at their trial stages. This is also in case all their trials are advancing at each stage, as in the other graphs; take this with a grain of salt.

This graph accounts for the current Phase II drugs’ advancement into Phase III, as I have outlined above. Funding this would be incredibly difficult and likely dilute shareholders.

This graph depicts potential acquisition prices for Coherus at each stage.

If Coherus tries to fund these trials itself, it would, if even possible, significantly dilute shareholders.

.

For oncology, to fund their trials, Coherus would likely need to raise USD 10-20M per Phase II trial and USD 50-100M per Phase III trial. Since they are currently conducting four Phase I trials and 2 Phase III trials, the total cost to fund all their trials would likely exceed USD 400 M+. It's hard to pinpoint exact numbers here, and the new FDA Optimus design doesn’t make this easier.

If they can progress most of their trials, they might be able to raise capital without diluting too heavily.

As you can see, the complete Phase II advancement alone could put the company at around USD 2B in market cap, causing necessary equity raising to fund corresponding trials of about USD 40M (Avg. cost), which would keep dilution under control at this stage when it comes to R&D. For the total Phase III advancement Avg. cost per trial is at USD 50-100M, so 6 x 100M on the high end, also because of the new FDA trial design, we would get USD 600M in cost, which could mean dilution % = $0.6 Billion / $5.6 Billion → Dilution % = 0.1071, or 10.71%.

Now, even though these are cumulative across all trials, we can use these numbers to estimate the average dilution cost per Phase II trial at 2-5% and per Phase III trial at 10%, while commercialisation might cut as high as 20-40%, depending on the amount of drugs and peak-sales commercialised.

Expected ROI

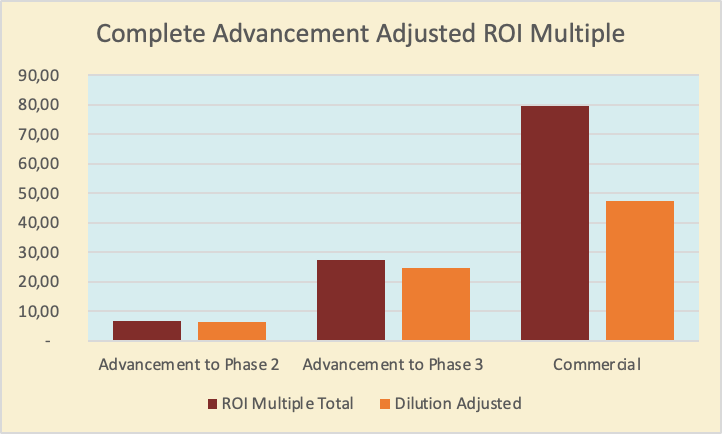

In the face of the graph above, the buyout value would be the multiple of the market cap at trial advancement above, minus dilution and plus premium.

Below, I have plotted the potential multiple on your investment if all trials advance at each stage, next to the dilution. In this graph, you can clearly see why finding a licensing partner or an acquisition might be very beneficial to avoid the heavy Phase III marketing dilution.

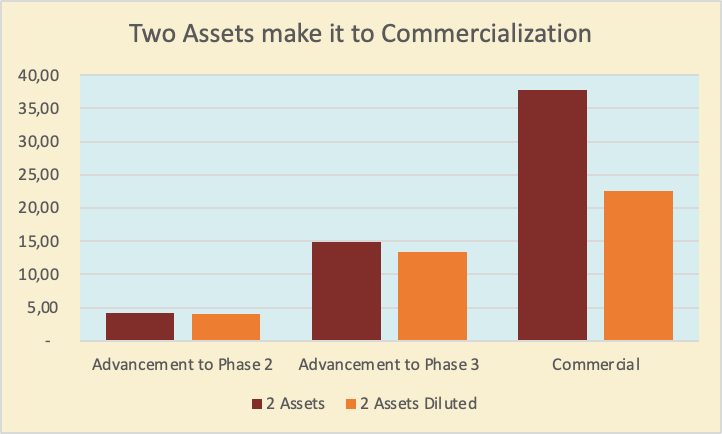

Below, I plotted a similar scenario in the case of only 2 drugs advancing. This is more likely than the above scenario at about 60-70% due to the sheer amount of drugs in their pipeline.

Something I really like about Coherus is that even in a complete trial failure, there is at least some valuation floor because of LOQTORZI.

Now I value this investment more than other Biotech investments. Coherus has incredible strengths, but also some weaknesses, like the CEO. In my quality-, dilution- and time-adjusted multiple, Coherus is valued at 3.4x its current value. This is largely due to a revenue peak occurring 9 years ago, discounted at my personal WACC, the PoS and the Management discount I discussed above.

This multiple is especially important if you have a diversified Biotech portfolio, since Biotech is time-dependent.

Key Risks

Trial Failure. Failing a trial is very likely. Coherus has shown promising data, but trial design can still fail, and sometimes using a larger sample size can change study outcomes.

Dilution. Even in trial successes, dilution is likely and always a risk, especially at the current market cap.

Competition. Oncology is a competitive sector. If Coherus enters the commercial stage, there is always the risk that a competitor will launch a better product, which would hurt Coherus’ outlook.

Entry

In light of the current geopolitical situation, especially the ultimatum to Iran, I would wait at least until the deadline (tonight at 8 pm) before entering the stock market. I think the event will be bipolar only downward in the short run, with the upside coming further in the future, since there will be no quick end to the shortage of oil, as well as the whole international landscape moving toward closer ties with Iran, as for example, India looking for an oil deal. Any downturn in the stock market can significantly increase your ROI, especially given this market cap.

Further, since the CEO has undershot expectations for their LOQTORZI sales, non-profitable biotech companies are usually negatively affected by 10-Qs. Another strategy would be to wait until their 10-Q release, then enter a position.

Exit

As I depicted above, when exiting, I would consider the dilution probability. This also depends heavily on how many drugs they can retain in their pipeline, with more drugs requiring more dilution, since LOQTORZI could pay for a larger share of the required capital if they have fewer drugs to commercialise. Although a USD 175M may not make a huge difference when you need USD 1B+ for marketing.

In case of a buyout in Phase II, this question is redundant.

Conclusion

Should you buy Coherus? CHRS is a strong buy if you have a Biotech or growth portfolio that is well-diversified. The potential returns are really high, and the downside is buffered by LOQTORZI.

If you are not diversified, do not buy Coherus, as trials can fail; for example, the chance of a Phase I trial advancing to the commercial stage is about 10%.

I give Coherus a Pluto Value (I created it, so I will name it) of 3.4x, which is close to its DCF fair value at a share price of USD 4.7.

Enter after the deadline tonight, or after earnings, or in two instalments.

If you read until here, you are exactly what this account is for. Please consider the following.

Thank you for this post!